Why Insurance Claims Get Underpaid | Florida Public Adjuster Help

Discover why insurance claims may be underpaid and how a licensed public adjuster can help Florida homeowners review and strengthen their claim.

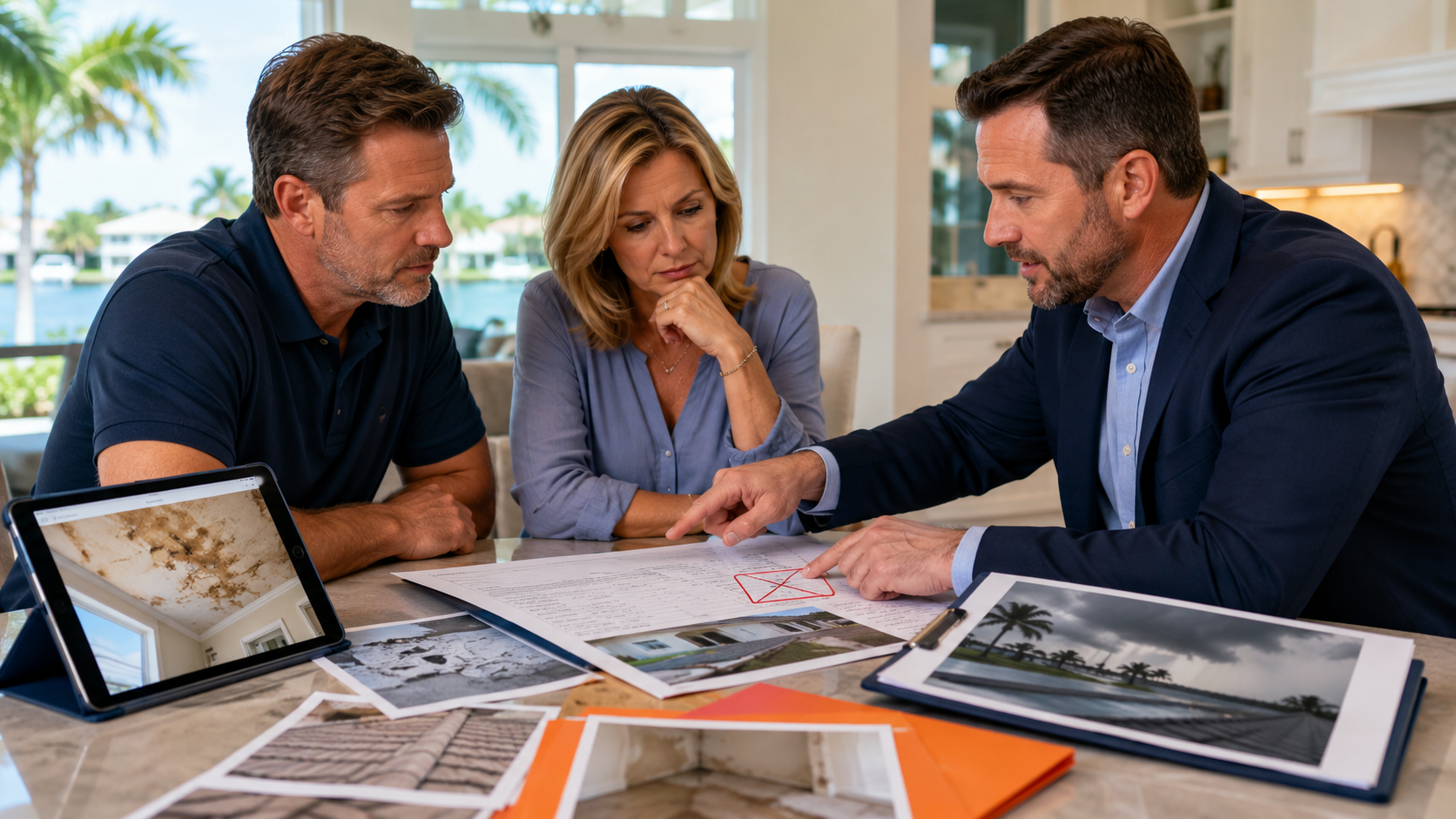

Underpaid Claims

Receiving an insurance payment after property damage should bring relief. But for many homeowners, the first settlement offer feels too low to cover the actual cost of repairs.

This is a common frustration. A homeowner may have roof damage, water damage, storm damage, or interior repairs that seem much more expensive than what the insurance company is offering. When this happens, the claim may be underpaid.

At The Claim Company, we help Florida homeowners review underpaid claims and understand what may be missing from the process.

What Is an Underpaid Insurance Claim?

An underpaid claim happens when the insurance company offers less than what may be needed to properly repair covered damage.

This does not always mean the claim was intentionally handled unfairly. Sometimes an underpaid claim happens because damage was missed, documentation was incomplete, or the scope of repairs was not fully evaluated.

However, if the payment is not enough, homeowners should not ignore it.

Common Reasons Insurance Claims Are Underpaid

1. Damage Was Not Fully Documented

Insurance claims depend heavily on documentation. If the damage is not photographed, measured, explained, or supported properly, the insurance company may not include everything in the estimate.

For example, water damage may affect flooring, baseboards, drywall, cabinets, and hidden areas. If only the visible water stain is documented, the estimate may not reflect the full scope of repairs.

2. Hidden Damage Was Missed

Not all damage is obvious at first glance. Roof damage, moisture behind walls, mold growth, structural issues, and interior leaks may require a more detailed inspection.

If hidden damage is not identified early, the claim payment may only cover surface-level repairs.

3. The Insurance Estimate Is Too Limited

Insurance companies often prepare their own repair estimate. That estimate may not always match the real cost of labor, materials, permits, code requirements, or the full scope of damage.

A limited estimate can leave the homeowner paying out of pocket for repairs that may be connected to the claim.

4. Policy Coverage Was Not Fully Reviewed

Insurance policies contain coverage details, exclusions, limits, deductibles, and conditions. If the policy is not reviewed carefully, important coverage may be overlooked.

A public adjuster can help review the policy and compare it to the damage being claimed.

5. The Cause of Damage Was Disputed

The insurance company may question whether the damage was caused by a covered event. For example, roof damage may be described as wear and tear instead of storm-related damage.

When the cause of damage is disputed, strong documentation becomes even more important.

6. The Homeowner Accepted the First Offer Too Quickly

After a stressful loss, many homeowners simply want the situation resolved. But accepting the first offer too quickly can be risky if the full damage has not been reviewed.

Before signing documents or closing a claim, homeowners should understand whether the offer truly reflects the damage.

Signs Your Claim May Be Underpaid

Your claim may need a closer review if:

- The settlement does not cover repair estimates

- Your contractor finds additional damage

- The insurance estimate seems incomplete

- Important rooms or materials were left out

- The damage keeps getting worse

- Your claim payment feels much lower than expected

- The insurance company is not explaining the offer clearly

If any of these apply, it may be time to speak with a licensed public adjuster.

How The Claim Company Helps With Underpaid Claims

The Claim Company helps homeowners by reviewing the claim, inspecting the property, organizing documentation, and identifying issues that may have been missed.

Our support may include:

- Reviewing the insurance estimate

- Inspecting the damage

- Comparing the scope of damage to the settlement

- Helping prepare stronger documentation

- Communicating with the insurance company

- Advocating for a fairer claim outcome

We work for the homeowner, not the insurance company.

Why Homeowners Should Not Wait Too Long

Insurance claims may involve deadlines, policy conditions, and documentation requirements. Waiting too long can make the process harder.

If you believe your claim was underpaid, it is better to request a review as soon as possible.

An underpaid claim can leave homeowners frustrated, confused, and financially stressed. But you do not have to accept a low offer without understanding your options.

If your insurance payment does not seem enough to repair the damage, The Claim Company can help you review the claim and take the next step with confidence.

Think your insurance claim was underpaid? Contact The Claim Company today for a free claim review.

Underpaid Insurance Claim, Underpaid Claim Florida, Public Adjuster Florida, Insurance Claim Dispute, Low Insurance Settlement, Property Damage Claim, Roof Damage Claim, Water Damage Claim, Storm Damage Claim, Homeowners Insurance Claim

#UnderpaidClaim #InsuranceClaimHelp #PublicAdjusterFlorida #FloridaHomeowners #LowInsuranceSettlement #PropertyDamageClaim #HomeInsuranceClaim #ClaimReview #InsuranceClaimDispute #TheClaimCompany